The turnover at L&L Partners’ corporate partnership (excluding the separate litigation and other partnerships) had increased by 12% between the 2018-19 and the 2019-20 financial years, revealed court filings by senior partner Mohit Saraf in the Delhi high court dispute with managing partner Rajiv Luthra.

However, not all was necessarily rosy from a financial side, as Saraf predicted a Rs 20 crore financial hole due to the end of a large mandate, and the loss of Rs 34 crores of billings due to partner exits (read on for more information).

The pleadings, a softcopy of which we have seen after they have begun circulating in wider legal circles outside the firm, include more than 700 pages of annexed discussions about equity dilution and other crises via WhatsApp and email, partnership deeds, termination notices, as well as a transcript of the infamous Zoom townhall by Luthra in late September.

As revealed in court on 22 October by Saraf’s counsel, the entire L&L-brand firm has had a turnover of around Rs 250 crore ($34m). That figure included all the corporate partnerships - which had been co-founded by Luthra and Saraf in 1999 - as well as the litigation, tax and intellectual property (IP) partnerships.

But unlike the foreign legal market, there has been very little transparency in revenue figures of Indian law firms (besides our report of Khaitan & Co turnovers having topped Rs 600 crore).

Now, the WhatsApp conversations between Luthra and Saraf annexed to the court pleadings have provided further insight into the size and profitability of one of India’s largest corporate law firm businesses, as well as other interesting insider information.

Tomorrow (Friday, 6 November), the Delhi high court will again hear Saraf's counsel arguing for an injunction against Luthra, to reinstate him into the firm.

Here is what’s at stake.

Structural context

For context, before getting too deeply into the weeds, there are at least six L&L Partners-branded entities. Internally at L&L, these are often referred to as L1 to L4:

- L2 is the corporate partnership, co-owned by Luthra (with a 66.6% stake) and Saraf (33.4%).

- L3 is the L&L Partners-branded litigation partnership that also includes three other equity partners. In this, Luthra is the largest single equity holder with 23.35%, while Saraf owns 11.12%. Another 18.51% each are held by HS (Bobby) Chandhoke, Sudhir Sharma and Vijay K Sondhi (and another 10% is held by partner Deepali Chandhoke, who is also the spouse of HS Chandhoke).

- L4 is the separate corporate partnership that just includes the firm’s Mumbai office.

- tax and IPR are two more L&L-branded partnerships for each respective practice area, each with separate deeds.

- L1 is included here mostly for historical reasons, as it is the Rajiv Luthra-owned sole proprietorship Luthra & Luthra Law Offices from the early 90s, which predates the 1999 partnership between Luthra and Saraf. Technically L1 still exists, though operationally the brand name, revenues and overall business have been assigned to the other partnerships.

The financial data below primarily concerns the corporate partnerships (L2 and Mumbai’s L4, in some cases).

2018-19 corporate revenues: Rs 147 cr; profits: Rs 43 cr

According to a WhatsApp message by Luthra to Saraf in May of 2020:

- in 2018-19 the “adjusted corporate turnover... (after adjustment tax/IPR and L-3)" (see below) was Rs 147.15 crore (around $20m).

- “Adjusted Corporate Profit" for that year was Rs 43.2 crore (around $6m), according to Luthra’s message.

Those figures are equivalent to a profit margin of around 29%.

In line with his 66.6% equity share in the corporate partnership, Rajiv Luthra then said that his profit share for 2018-19 was Rs 28.8 crore (around $3.9m), while Saraf’s share was the remaining Rs 14.4 crore (around $1.9m).

Luthra had sent the above message in the course of a longer WhatsApp conversation with Saraf about the future of the firm, notably with Luthra proposing to dilute some equity in exchange for a 7.5% share of the top line revenues for Luthra (i.e., off the revenues before the deduction of any expenses).

But 2018-19 may also have been an unusually profitable year for corporate.

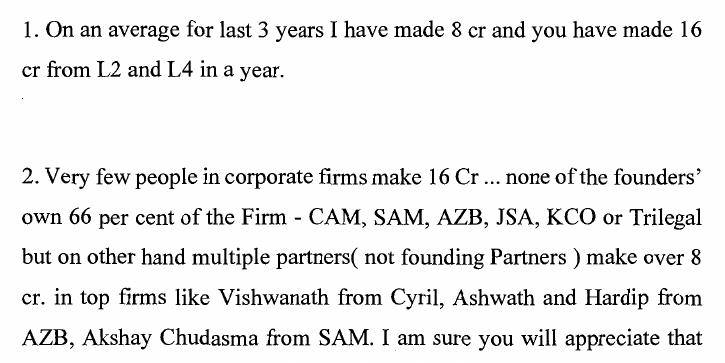

In December 2019, Saraf wrote to Luthra via WhatsApp that “on an average for last 3 years I have made 8 cr and you have made 16 cr from L2 and L4 in a year”.

PEP: Amongst top 30 US firms

If you were to convert Luthra and Saraf’s 2018-19 profits paid to profits per equity partner (PEP), which is a measure often used in international legal markets to measure a law firm’s profitability, it would put just the corporate partnership (excluding litigation) PEP at $2.9m.

That would put L&L amongst the top 30 US international firms' PEP figures, though it would still be less than the $6.3m that an average one of 85 Wachtell Lipton Rosen & Katz partners take home.

With the litigation partnership, Saraf and Luthra’s yearly profits may be even higher.

Going by the Rs 16 crores profits that Luthra had apparently taken in 2018-19, Saraf argued in December 2019 in a series of messages about diluting their equity that they were both outliers in the Indian market.

“Very few people in corporate firms make 16 Cr,” wrote Saraf. “None of the founders’ own 66 per cent of the Firm - CAM, SAM, AZB, JSA, KCO or Trilegal but on other hand multiple partners (not founding Partners) make over 8 cr. in top firms like Vishwanath from Cyril, Ashwath and Hardip from AZB, Akshay Chudasma from SAM.”

Saraf’s argument was that without the two giving up more equity, L&L would not be able to attract and retain star talent.

He also added that his own contribution to L&L was surely therefore of a greater value than Rs 8 crores.

2019-20 corporate revenues: Rs 167 cr

Around June 2020, Saraf wrote to Luthra that in the 2019-20 financial year the corporate revenue in the corporate Delhi partnership (L2) in 2019-20 was Rs 111 cr.

The Mumbai office corporate partnership (L4) was Rs 56 cr that same year.

Combining both of those gives a 2019-20 overall corporate firm revenue of Rs 167 cores (around $22m).

Overall, for both corporate partnerships together, that represents a year-on-year turnover growth of around 12%.

Saraf was quoting the figures in order to demonstrate that under Luthra’s stewardship the Delhi office had grown much less rapidly than the Mumbai office and partnership, which Saraf had managed.

Saraf noted that since 2008-09 the Delhi (L2) partnership had grown from Rs 80 cr then its average annual growth rate until 2020 equated to only 3.06% per year (comparing unfavourably to “the Indian economy [...] growing at 7%“, according to Saraf).

By contrast, claimed Saraf, the Mumbai office that he himself had set up and managed had grown from Rs 9 cr in 2008-09 (or by 18.09% year-on-year).

Saraf's predictions for 2020-21 dire: Hole of Rs 62 cr

Saraf then continued arguing that the outlook for 2020-21 was not good and that Luthra’s dilution offer would not work commercially for the firm as a whole.

“After, spending a couple of days and many hours in discussion with our partners, Mr. Luthra one thing is very clear,” Saraf wrote. “Pre-covid and Post-Covid, the worlds are completely different.

“The uncertainty quotient in business is looming large in the post Covid world and I won’t be surprised if the Firm incur operating losses 20-21 and 21-22.”

In particular, he pointed to several factors that would put financial stress on the firm, not just related to Covid.

In particular, the loss of the books of business of five partners could cost the firm Rs 42 crores in revenues, he argued, while the end of the ArcelorMittal insolvency would hit revenues by Rs 20 crores.

“They [partners] are cognisant that Insolvency work (25 crore) which was a key driver of revenue (especially ArcelorMittal - 20 cr) would be dried up. Alina’s (10 cr), Manan’s (12 cr), Sameen’s (8 cr), Amit Shetye (7 cr) and Aditya Periwal (5 cr) departure would have added to the hole,” wrote Saraf, adding: “Covid has dramatically altered prospects in the near to middle term.”

Of these:

- Alina Arora joined Shardul Amarchand Mangaldas,

- Amit Shetye went in-house to GIP,

- Aditya Periwal joined AZB, and

- Manan Lahoty went to IndusLaw with 17-fee-earners including partners.

Senior projects partner Sameen Vyas had passed away in October 2019.

Saraf also predicted that profitable practices from other partners would come under pressure from rival firms looking to poach them if the firm did not adjust its equity model and retention strategies.

Saraf mentioned nine corporate partners in particular, across two teams - Bikash Jhawar’s team of five partners, and the team consisting of Vaibhav Kakkar, Sundeep Dudeja and one more partner - as accounting for a total revenue of Rs 55 crore.

Those two corporate teams had made up 50% of both Mumbai and Delhi corporate partnership revenues and a whopping 60% of profits, according to Saraf.

Luthra declined to comment on the accuracy of the figures, and Saraf did not respond to a request for comment.

threads most popular

thread most upvoted

comment newest

first oldest

first

Mohit was warned at multiple levels that Manan is planning an exit. Please read the chats - Manmeet Singh had specifically sounded off Mohit of Manan's departure, BEFORE the story actually broke. So it is patently false to say that RKL and MS found out through legally India. If you read the chats, you can sense the desperation in MS' texts to RKL to try and stop Manan BEFORE the story hit the press.

Secondly, with respect to Alina, again please read the chats. There is a clear sense of betrayal amongst the Partners at how her exit and that of the bulk of her team was engineered by her. One of the EC members goes on to say that at least Manan was upfront in his intentions from day 1, whereas Alina proclaimed something and did something else (read: poach the bulk of her team). RKL goes on to express his dismay that he let her phone number continue with her on the representation that she was retiring for personal reasons.

So the hurt was as much as at the time of Manan's departure.

Factual correction: Alina's team was 7 strong (including her).

She joined SAM during the lockdown almost 5 months after legallyindia reported her resignation. There was no reputational loss (lol) to Luthra when Alina left - hence, pleasant exit. And only half her team went with her - last I checked some of her team are still working here in Luthra Delhi.

Then again, RKL probably set the relationship up years ago but left partners, including Alina and certain others, to keep such clients happy and ensure they kept coming back. So no taking that away.

manan- capital markets which is such a vanity practice in india not just in luthra. as it takes lots of resources and does not earn up enough.

“Very few people in corporate firms make 16 Cr,” wrote Saraf. “None of the founders’ own 66 per cent of the Firm - CAM, SAM, AZB, JSA, KCO or Trilegal but on other hand multiple partners (not founding Partners) make over 8 cr. in top firms like Vishwanath from Cyril, Ashwath and Hardip from AZB, Akshay Chudasma from SAM.”

Its ok bhai saab.

Hugs

Kisses.

Can't RKL and MS take a cue out of this also?

Shameful, classless behaviour to say the least. He should take his two cents and get lost!!

Can agree with you on one thing. He is going to leave. Once this is sorted - he will obviously not be a part of L&L, along with a lot of sensible people and clients.

Thanks.

You read "crores" & get impressed

You're from a top NLU. Smart. Willing. ....So f***ing what!

Reality dear child:

1. Almost 0% will touch 1cr after 10 yrs of 24x7 work

2. Only 2-3% will come close to 1cr after 12-13 yrs of 24x7 work

3. Meanwhile life will take its toll

Please plan your life

Don't behave like like poultry in a mandi

PS. Entry of any Foreign Firm is not going to save you

Also, comparison in lit and corp at later stage is futile. If you are successful, your time is equally valued in both. However, probability of making it to the 4-8 Cr revenue in dependent on probability of you becoming a senior advocate in select courts. Same for corporate. Most do not make it to even 3 crore.

You can also do Litigation in a firm where work is shit, but you will make relatively equivalent pay - depends on firm to firm, but usually there’s a diff of 20-30 percent between corporate and Lit folks.

Working as an independent litigator is another ball game, depends which office your associated with, but broadly speaking don’t have any financial expectations till you’re 35. Even after that you can have lean phases. It’s impossible to predict a litigators financial journey.

Free advise - don’t take career advice on Legally India, and don’t compare how much you can make by looking at someone 20 years your senior - the examples you’ve cited. The world will fundamentally change by the time you’ve worked for 20 years, so be realistic of what you can predict. Even if you’re brilliant, you can still end up earning in 50 lakhs of so. Law firms / litigation success is dependent on luck and timing to a large extent, which people don’t talk about as it will overshadow their perception of their intelligence.

Ashwath: 12 crores

Chudasama : 12 crores

Raghubir Menon: 10 crores

Those whatsapp figures are outdated. Wonder if anil Kosturi and Gautam saha azb will resign in protest next.

Aur neend kaise aati hai - koi le gaya toh? :P

1) There is lot of double counting in the figures. Arcelor was handled by SV and a few other Partners, including from Mumbai who left. You don't count the hole due to Arcelor and also from the absence of these partners twice over. In fact Arcelor accounted for almost the entire billing of SV's team.

2) From what I heard, rumours of course in the firm, SV and Madhurima were both offered equity when Madhurima joined, but of their own teams ( a model rumoured to be followed at SAM perhaps). It was like the L2 created for MS. Madhurima refused as she wanted for the whole firm. SV took it up and regretted as his take home took a dramatic hit and he went back to Paid Partner in the boom boom years.

3) Manan's exit creates a hole in revenues and not profits as his team took home whatever revenue they generated.

4) [...]

1) A lot of the expenses incurred by the senior partners is on the expense account of the firm.

2) RKL has many personal retainerships of substantial worth, the payments for which do not come into the L2 account. Speculation is that it went into L1.

3) The billings by the senior partners is their personal change, not part of PnL of L2-4. In L2 annd L4, to get the matters referred to by senior partners one needed to bill for them for consultation at every stage of a matter which mattered.

For example- it’s shocking to hear that Luthra has lost almost a 35 crore book over the last year or so!!! That’s a lot of money!! Or for that matter Bikash and Sundeep/ Vaibhav’s team making 50% of the profits and 60% of the revenue. What are the other teams doing?!

Are they the new equity partners who Luthra have appointed?! I sure hope so- it would be stupid to not!!

The other corporate partners are really miles behind it seems if just 2 teams (and 8 partners) are contributing to more than 60% profit. What are the rest 25-30 of them doing?!

threads most popular

thread most upvoted

comment newest

first oldest

first